Why Awareness Beats Automation When It Comes to Budgeting

Why do budgeting apps feel great at first, then quietly stop working?

Most people assume better budgeting comes from better technology. If you’re struggling to manage money, the instinct is to download an app, connect your accounts, and let automation handle the rest. Sometimes that works well, and modern budgeting apps are genuinely powerful.

For a lot of people though, the problem was never a lack of features. The problem is consistency. You connect your accounts, transactions start flowing in, categories build themselves, and within minutes you have a dashboard full of charts. That part feels great.

Then a few weeks in, the checking-in stops. The information is still there, sitting in the app, but the habit of actually looking at it never quite forms. The app knows where the money went. The person using it still feels disconnected from it. That’s not really a flaw in the app, it’s a reminder that collecting data and paying attention to it aren’t the same thing.

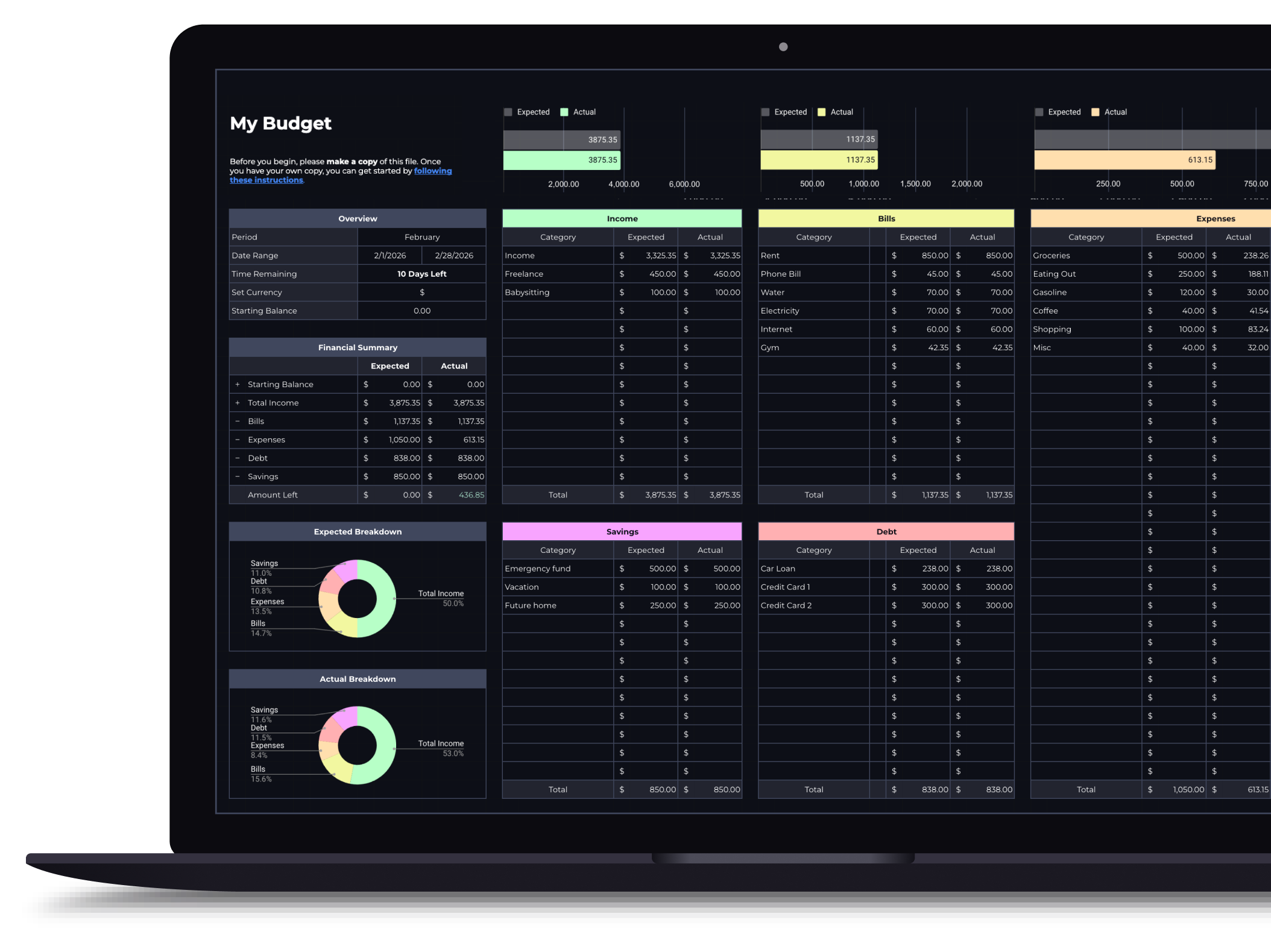

What does a spreadsheet do differently?

A spreadsheet doesn’t automate much. You decide the categories, you enter the transactions, you review the numbers yourself. That sounds like a disadvantage on paper, but for a lot of people it’s the actual reason a spreadsheet works.

When you manually type in a purchase, you notice it. A $14 lunch or a forgotten subscription is harder to ignore when you’re the one entering it, instead of letting an algorithm quietly file it into a category you never check. The small effort creates the awareness, which is the whole point.

![]()

There’s a visual difference too. An app spreads your financial life across multiple screens, tabs, and toggles. A spreadsheet puts it all on one surface, so you can open it and see your whole month at a glance instead of tapping through menus to find the number you’re after. For someone trying to build a daily or weekly check-in habit, that one flat view tends to matter more than people expect.

Why do simple systems tend to last longer?

Most budgets that actually stick aren’t built on motivation, they’re built on routine. Five minutes at the end of the day isn’t exciting, but it works. A weekly review isn’t revolutionary either, but it works too.

Simple systems are easier to turn into habits mainly because there’s less to manage. There’s no account connection to troubleshoot, no subscription to keep paying for, no settings menu to configure, just a place to record what’s happening and a reason to look at it regularly. The goal isn’t building the most advanced financial system possible, it’s building one you’re still using six months from now.

This is also where the anxiety piece comes in. It’s rarely the math that’s stressful, it’s not knowing. A system you update yourself tends to close that gap faster than a dashboard ever does, because you’re the one entering the number and you’re the one who watches the total move.

Does that mean a blank spreadsheet is the answer?

Not quite, and this is where a lot of “just use a spreadsheet” advice falls short. A blank sheet has its own version of the app problem: you have to build the categories, the formulas, and the layout before you can track anything at all. Most people give up right there, not because spreadsheets don’t work, but because building one from nothing is its own project.

The middle ground is a spreadsheet that’s already structured, but still just a spreadsheet. No login, no syncing, no algorithm guessing at what your coffee was. You open it, start typing in real numbers, and the structure is already there to catch them. That gets you the part that makes spreadsheets work, the visibility and the daily habit, without the part that makes them annoying, which is building one yourself from a blank tab.

The challenge isn’t tracking money, it’s building a system simple enough to keep using consistently. That’s also the question behind Where Is My Money Going?, if you’re still trying to figure out what your spending actually looks like before settling on a system.

Does cost factor into this at all?

It does, and it’s an underrated part of the comparison. Many budgeting apps run on a monthly or yearly subscription, which is worth it for people who lean on the automation. But not everyone needs that level of functionality just to stay aware of where their money is going.

A basic spreadsheet can be entirely free in Google Sheets, and even a pre-built budget template is usually a one-time cost rather than an ongoing one. For someone just getting started, that lower barrier alone can make it easier to begin, since there’s no account to connect and no new platform to learn.

So is a spreadsheet actually better than an app?

Not universally, and it’s worth being honest about that. Plenty of people use a budgeting app and would never switch back, and there’s nothing wrong with that. The deeper point isn’t spreadsheets versus apps, it’s awareness versus automation.

Apps automate the data. Spreadsheets tend to build awareness, simply because they ask a little more of you along the way. Neither approach is objectively better for everyone, but a lot of people underestimate how far a simple, visible system can go. The biggest improvement in most budgets doesn’t come from adding more features, it comes from actually paying attention, and the right tool is usually whichever one gets you to do that consistently.