What is the 50/30/20 rule? A simple way to split your paycheck

If you’ve ever wanted a budget but didn’t want to build one from scratch, the 50/30/20 rule is usually the easiest place to start. It’s not a strict system. It’s more like a compass: a simple split that tells you roughly where your money should be going, without asking you to categorize every coffee and Uber ride on day one.

What is the 50/30/20 rule?

The rule splits your take-home pay into three buckets: 50% to needs, 30% to wants, and 20% to savings and debt payoff. That’s the whole framework. No apps, no complicated tiers, just three numbers that add up to one paycheck.

It works because it gives you a direction without demanding precision right away. You’re not trying to get every category perfect in week one. You’re just checking whether your spending is roughly in the right zone, and adjusting from there.

What counts as a need versus a want?

Needs are the things you’d still have to pay for even if your income dropped tomorrow: rent or mortgage, utilities, groceries, insurance, minimum debt payments, transportation to get to work.

Wants are everything that makes life better but isn’t strictly required: dining out, streaming subscriptions, hobbies, travel, the nicer version of something you could buy cheaper.

Some categories sit in a gray area. A phone bill is usually a need, but the newest phone model upgrade is a want. Groceries are a need, but the $40 grocery run that’s mostly snacks and takeout substitutes leans toward want. When something feels ambiguous, a reasonable rule of thumb is to ask whether you’d cut it first if money got tight. If yes, it’s probably a want.

How do I find my own 50/30/20 numbers?

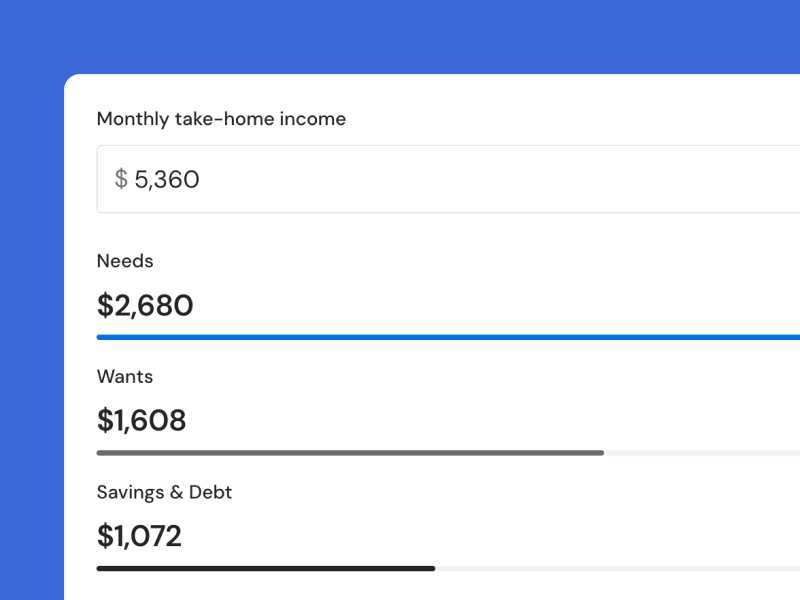

Start with your monthly take-home pay, meaning what actually lands in your account after taxes, not your gross salary. From there, the math is simple: half goes to needs, three-tenths to wants, and two-tenths to savings and debt.

If you’re paid every two weeks rather than once a month, add up two paychecks to estimate a typical month — then see how to budget when you get paid every two weeks for how to handle the months that bring a third paycheck.

To skip the math, use the calculator below. Enter your monthly take-home income and it will break out the dollar amount for each category.

Total: 100%

If your numbers don’t land cleanly in 50/30/20, that’s normal, especially in a higher cost-of-living area where needs can easily run past 50%. The ratio is a starting target, not a rule you’ve failed at. Some people land closer to 60/20/20 simply based on where they live, and that’s still a useful structure, just adjusted to reality.

What if my needs already take up more than 50%?

This is common, and it doesn’t mean the framework is broken. It usually means one of two things: either some genuine needs are higher than average for your situation, or some things currently labeled as needs are actually wants in disguise.

Worth checking before assuming you’re stuck: subscriptions that auto-renewed and got forgotten, a phone plan that’s larger than necessary, or a grocery budget that’s drifted upward without anyone noticing. None of these require a dramatic life change to fix, just a closer look at what’s actually landing in the needs column.

If after that the needs percentage still runs high, it’s fine to shift the ratio. A 60/20/20 or 55/25/20 split is still 50/30/20 in spirit: most of your money to needs, a smaller slice to wants, and a protected slice to savings.

Is 50/30/20 the actual goal, or just the starting point?

It’s worth being honest about this: 50/30/20 is a starting point, not a finish line. It’s a north star, something to aim for when you don’t have any other reference point yet. Once you’ve been budgeting for a while, the real goal shifts from hitting 50/30/20 exactly to gradually improving on it: nudging needs down and savings up as your situation allows.

In practice, that might mean working toward 45/30/25, then 40/30/30, over months or years, not overnight. Small, steady improvements to the ratio tend to matter more than getting the original split perfect. The number itself is less important than the direction it’s moving.

When does the 50/30/20 rule not work well?

The 50/30/20 rule assumes a fairly steady paycheck and a fairly average cost of living, and it bends or breaks in a few common situations.

Irregular income. If your income changes month to month, calculating 50/30/20 off a single paycheck doesn’t hold up. The percentages still apply, but they need to be applied to an averaged or baseline income rather than whatever happened to come in that particular month. For a full approach to this, see Budgeting with irregular income.

High cost-of-living areas. In expensive cities, needs alone can easily run past 50%, not because of overspending but because rent and basic costs are simply higher. The ratio still works as a concept, it just needs to be adjusted to something like 60/20/20 to reflect reality rather than treated as a failure.

Heavy debt situations. If minimum debt payments are large relative to income, the 20% savings and debt slice may need to temporarily grow well past 20% to make real progress, sometimes at the expense of the wants category. A debt-focused approach can make more sense than forcing the standard ratio. More on this is coming in a dedicated debt payoff article.

Couples managing money differently. Two incomes, shared expenses, and different spending habits make a single shared 50/30/20 split harder to apply cleanly. Some couples split by percentage of each income, others combine everything into one pool first. For a closer look at this, see the couples budgeting article (coming soon).

None of this means the rule is broken. It means it’s a flexible starting framework, not a rigid law, and adjusting it to fit your actual life is part of using it well.

How does this connect to actually tracking my spending?

The 50/30/20 rule tells you the target. It doesn’t tell you whether you’re actually hitting it, and that’s where most people’s budgets quietly fall apart. Knowing the numbers in theory and seeing them show up in your real spending are two different things.

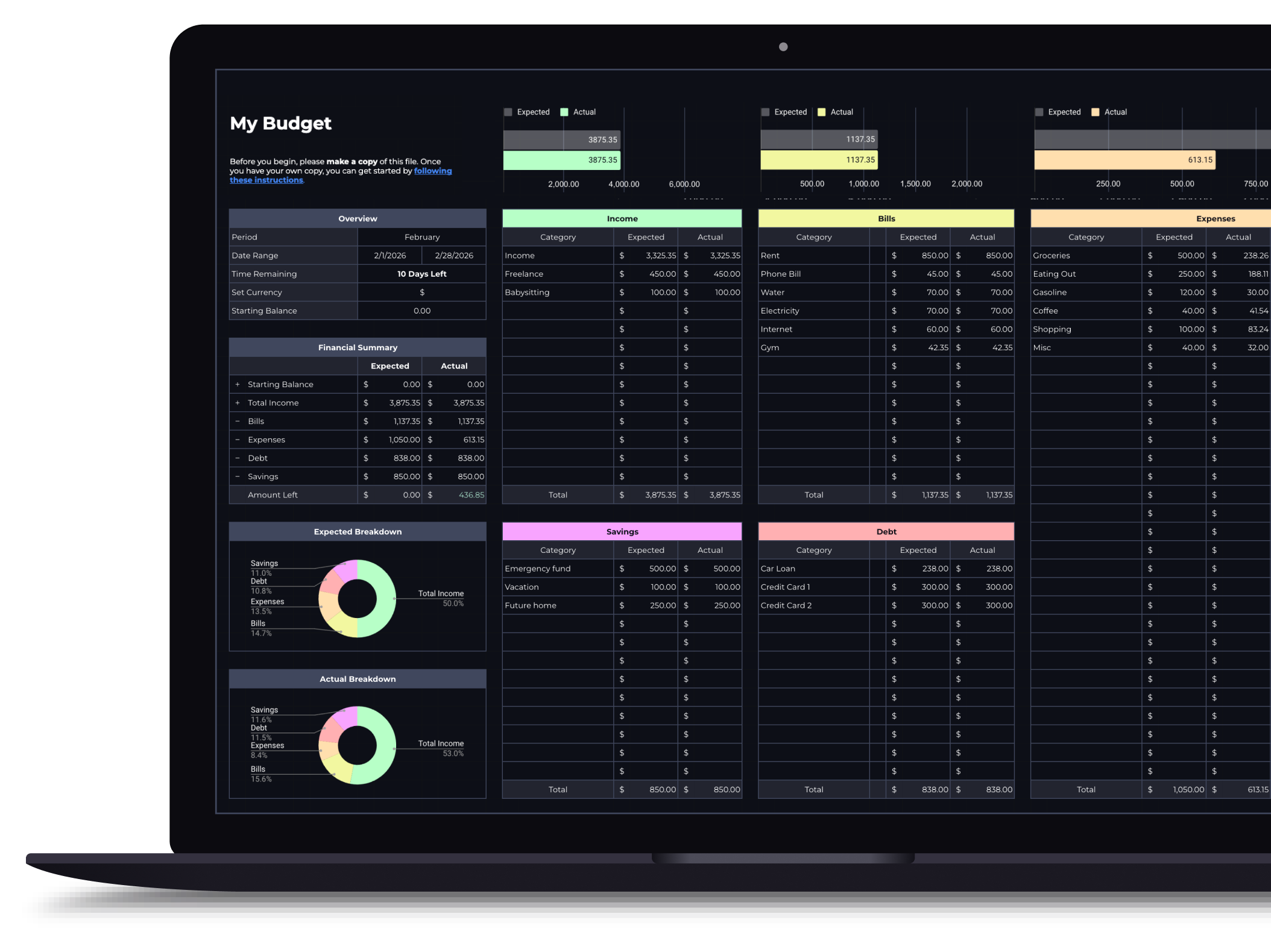

This is the gap a budget spreadsheet is built to close. Once you know your target numbers from the calculator above, a spreadsheet with an expense tracker lets you log spending as it happens and see, category by category, whether you’re actually landing where you planned. The calculator is the one-time math. The spreadsheet is what tells you the truth about every month after.

If you’re not sure where your money is going yet, start there first — tracking your spending for a few months will give you the real numbers to compare against your 50/30/20 targets.