The 4 Budgeting Styles: Which One Are You?

Most budgeting advice assumes everyone manages money the same way. They don’t. Some people feel calm when every dollar has a job. Others feel calm when they stop looking at their bank account altogether. In our experience, most people tend to lean toward one of four broad budgeting styles: Planner, Saver, Spender, or Avoider. Most people show traits of more than one depending on the situation, but one style usually feels more natural than the others.

The problem usually isn’t a lack of discipline. It’s using a budgeting system that doesn’t fit how you naturally think about money. A method that feels motivating to one person can feel exhausting to someone else.

Here’s what each style looks like, and what tends to trip each one up.

The Planner

Planners like having a system and knowing exactly where their money goes. Structure brings confidence, and things feel most under control when every dollar is accounted for in advance. The strength here is discipline. The challenge is staying flexible when life doesn’t follow the plan.

If this sounds like you, try scheduling a monthly budget review to adjust your plan based on actual spending instead of projected spending. A budget that adapts is one that lasts.

The Saver

Savers are naturally frugal and feel best watching their savings grow. Saying no to impulse purchases comes easily. The risk is holding back on things that would genuinely improve daily life, not just on things that don’t matter.

If this is your style, try setting aside a small amount each month as guilt-free spending money. Saving is the goal, not the whole picture.

The Spender

Spenders tend to prioritize experiences and immediate enjoyment. Money often feels like a tool for improving life today, not just something to save for the future. This often comes with generosity and spontaneity, which makes life more enjoyable. The challenge is building habits that balance today’s enjoyment with tomorrow’s stability.

A useful starting point is the 24-hour rule: wait a day before buying anything non-essential over $50. If it still feels worth it tomorrow, it probably is.

The Avoider

Avoiders tend to put off financial decisions because money causes stress. This is far more common than people assume, and small steps tend to work better than trying to overhaul everything at once.

The simplest place to start is checking your bank balance every morning, nothing more. Familiarity lowers anxiety over time, and that’s usually the real barrier, not the numbers themselves.

Most people aren’t just one type

Most people aren’t 100% one budgeting style. You might be a Planner when it comes to paying bills and a Spender when it comes to travel. The goal isn’t to put yourself in a box. It’s to understand which tendencies show up most often so you can build a system that works with them instead of against them.

Why knowing your budget type matters

Budgeting advice often fails not because the advice is wrong, but because it doesn’t match how the person actually thinks about money. A detailed, category-by-category system might feel reassuring to a Planner and completely overwhelming to an Avoider. A strict savings goal might motivate a Saver and feel punishing to a Spender. Matching the system to the person, instead of forcing the person to fit the system, is usually the difference between a budget that sticks and one that gets abandoned by February — it’s one of the most common reasons budgets fail in the first place.

Budgeting styles also collide when two people share money. If you and a partner land on different styles, budgeting as a couple without fighting about money covers how to build a shared system that works for both of you instead of forcing one style on the other.

Not sure which one you are?

Take the 60-second quiz

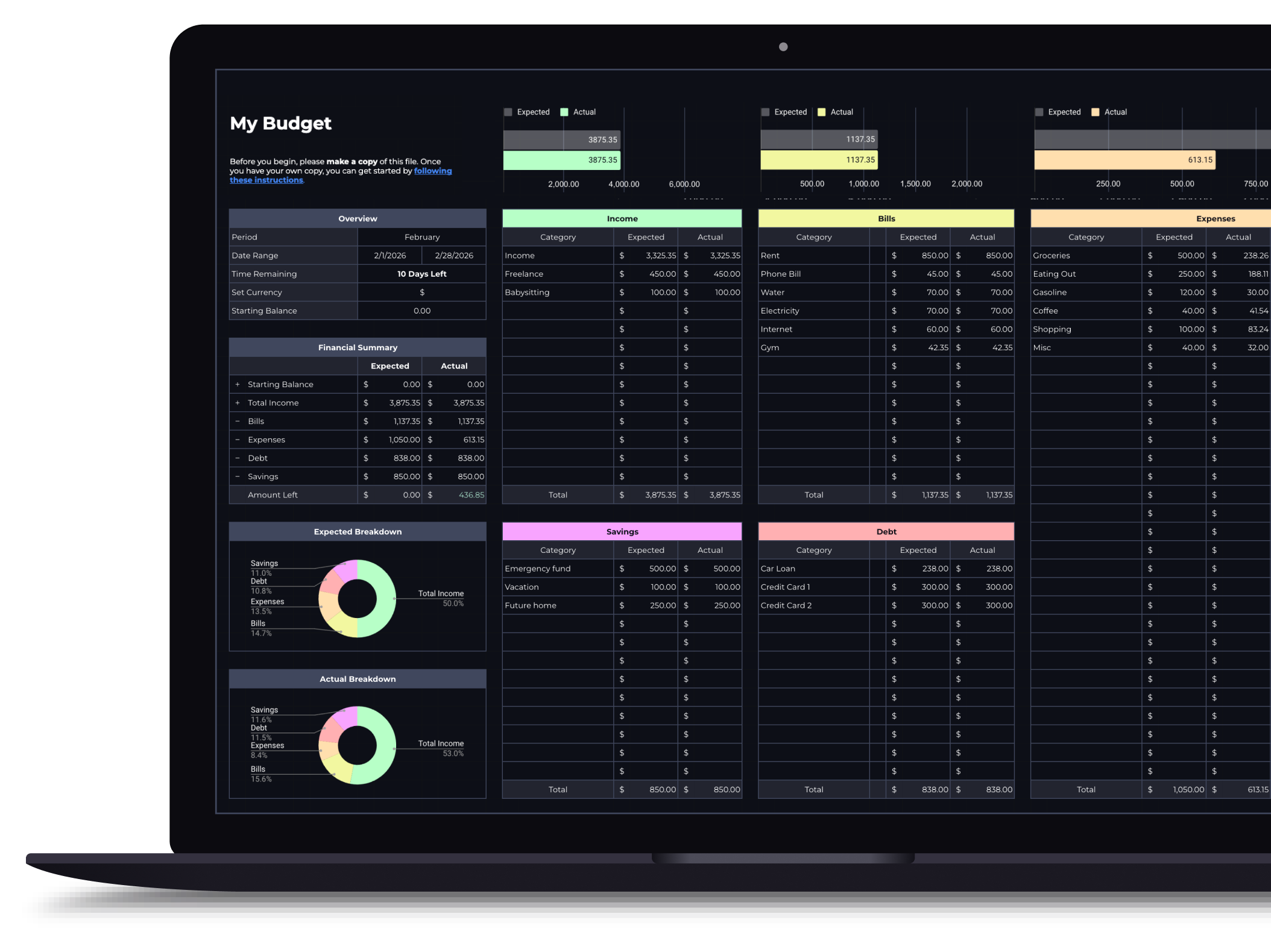

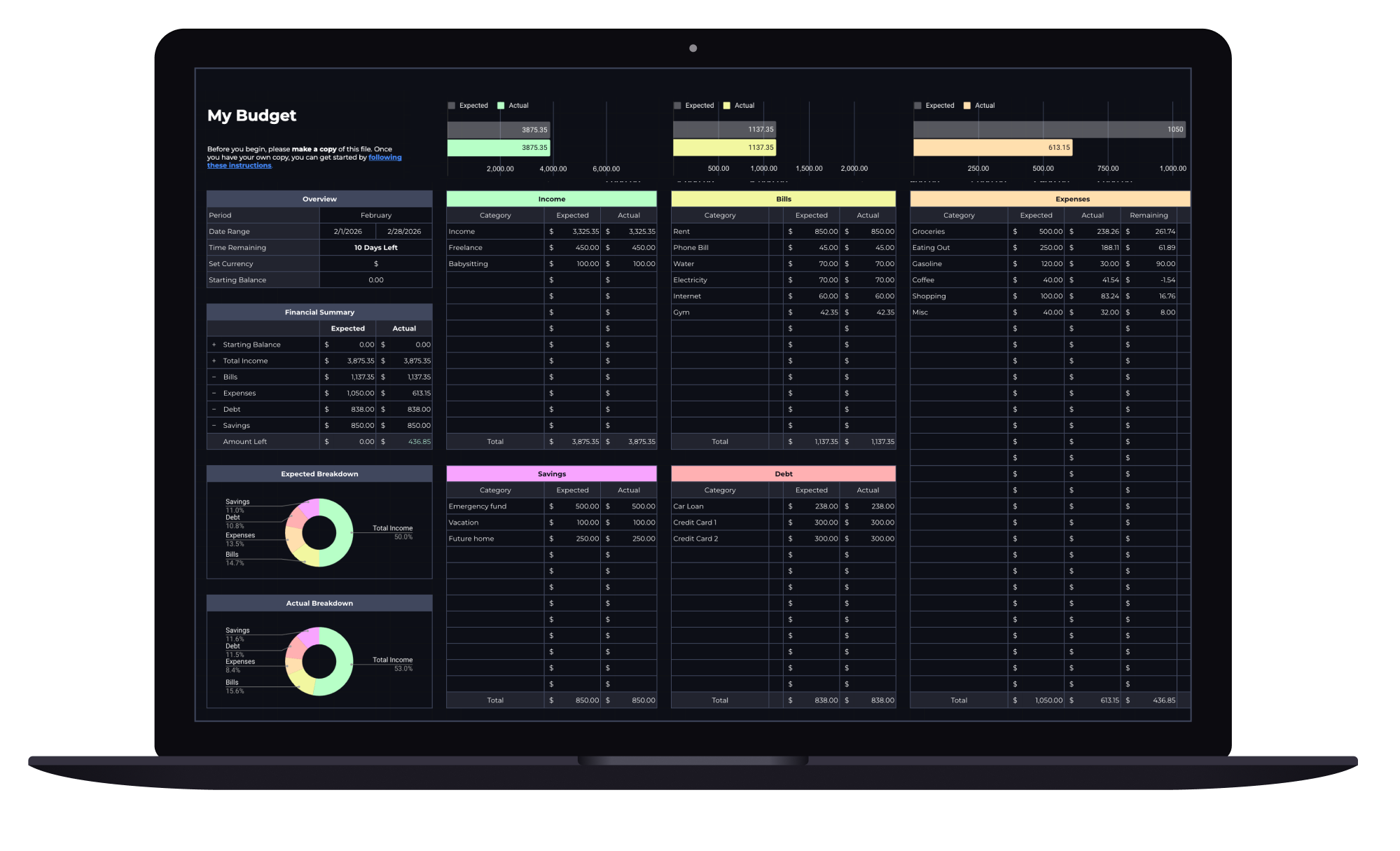

Budget Spreadsheet

Track your income and daily expenses with real-time progress indicators that show exactly where you stand each month. Works with Google Sheets and Microsoft Excel.

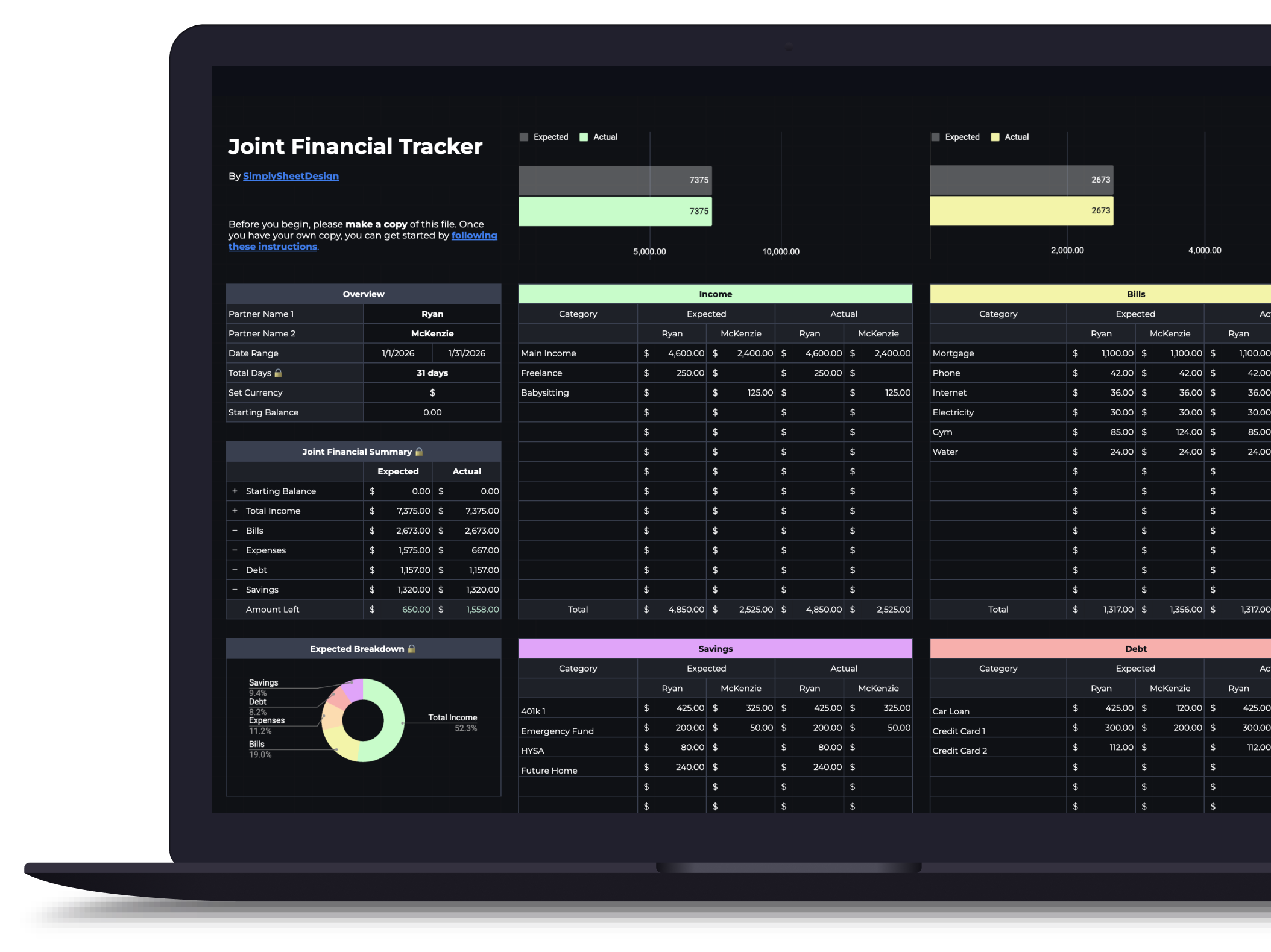

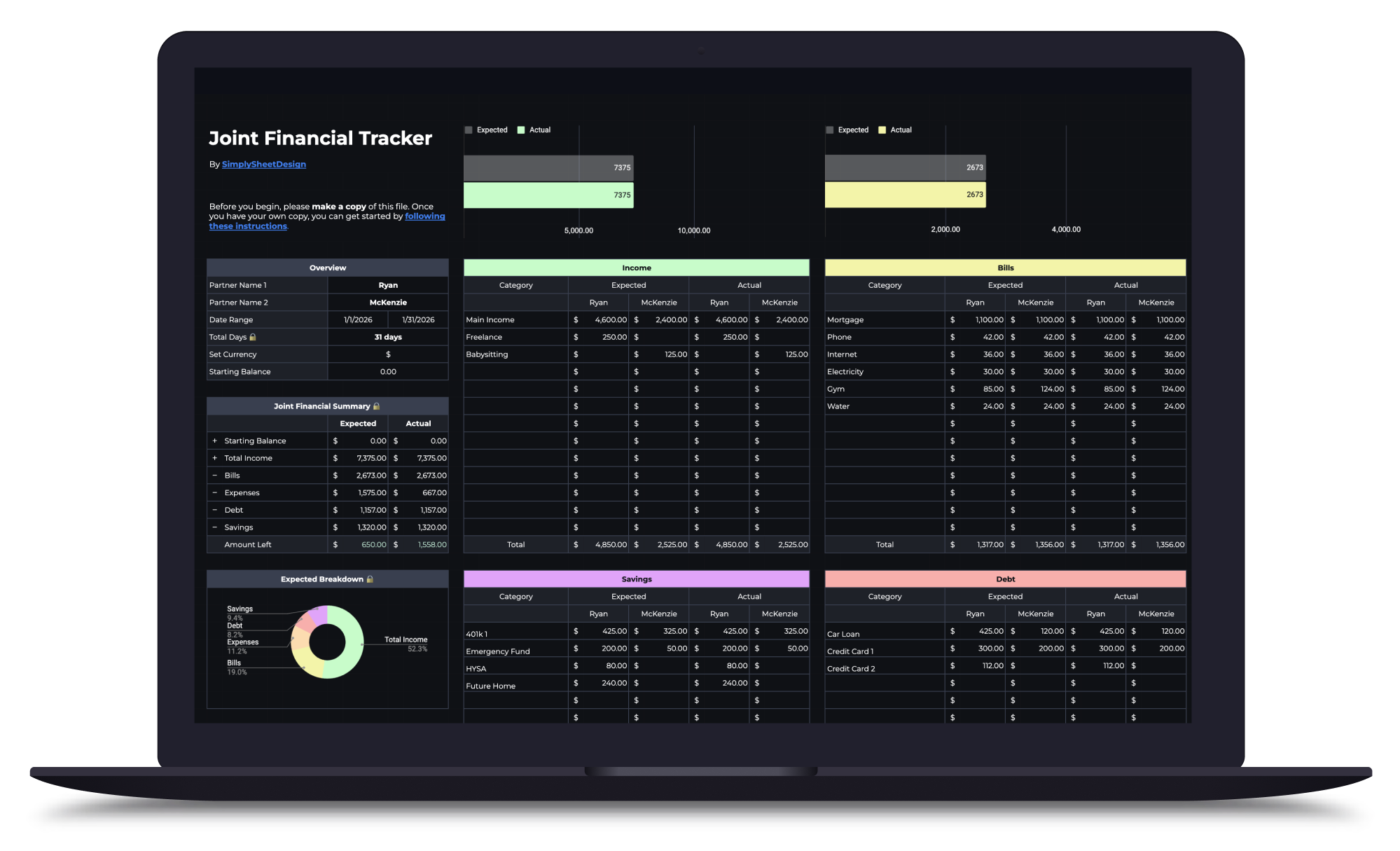

Couples Budget Spreadsheet

Split bills, track shared and personal expenses, and manage savings together. Built for two incomes, one shared financial picture.