Track Your Expenses for 30 Days Before You Build a Budget

Most people think the first step to budgeting is creating a budget.

For many people, that’s actually the second step.

Imagine two people deciding to get their finances under control. The first opens a blank spreadsheet and starts assigning numbers to groceries, restaurants, shopping, gas, and entertainment. Most of those numbers are educated guesses.

The second person doesn’t budget at all during the first month. They simply write down every expense.

Thirty days later, one person has a budget based on assumptions. The other has a budget based on reality.

That’s usually the better place to start.

Why do so many first budgets feel unrealistic?

The hardest part of building a budget isn’t choosing categories. It’s knowing what belongs in them.

Most people underestimate certain expenses, forget irregular purchases, or base their numbers on what they hope they’ll spend instead of what they actually spend.

None of those mistakes come from being careless. They happen because it’s difficult to plan accurately without first understanding your own spending patterns.

A month of expense tracking gives you that understanding before you ever have to decide how much should go into each category.

What should you actually track?

Much less than most people think.

You don’t need detailed notes about every purchase or complicated financial reports. For most people, three pieces of information are enough:

- The date

- The amount

- A simple category

That’s it.

The goal isn’t building perfect records. The goal is building awareness. If you’re not sure where to begin, Where Is My Money Going? walks through a simple approach to finding out.

Broad categories usually work better than highly detailed ones. Groceries. Restaurants. Transportation. Shopping. Bills. Entertainment.

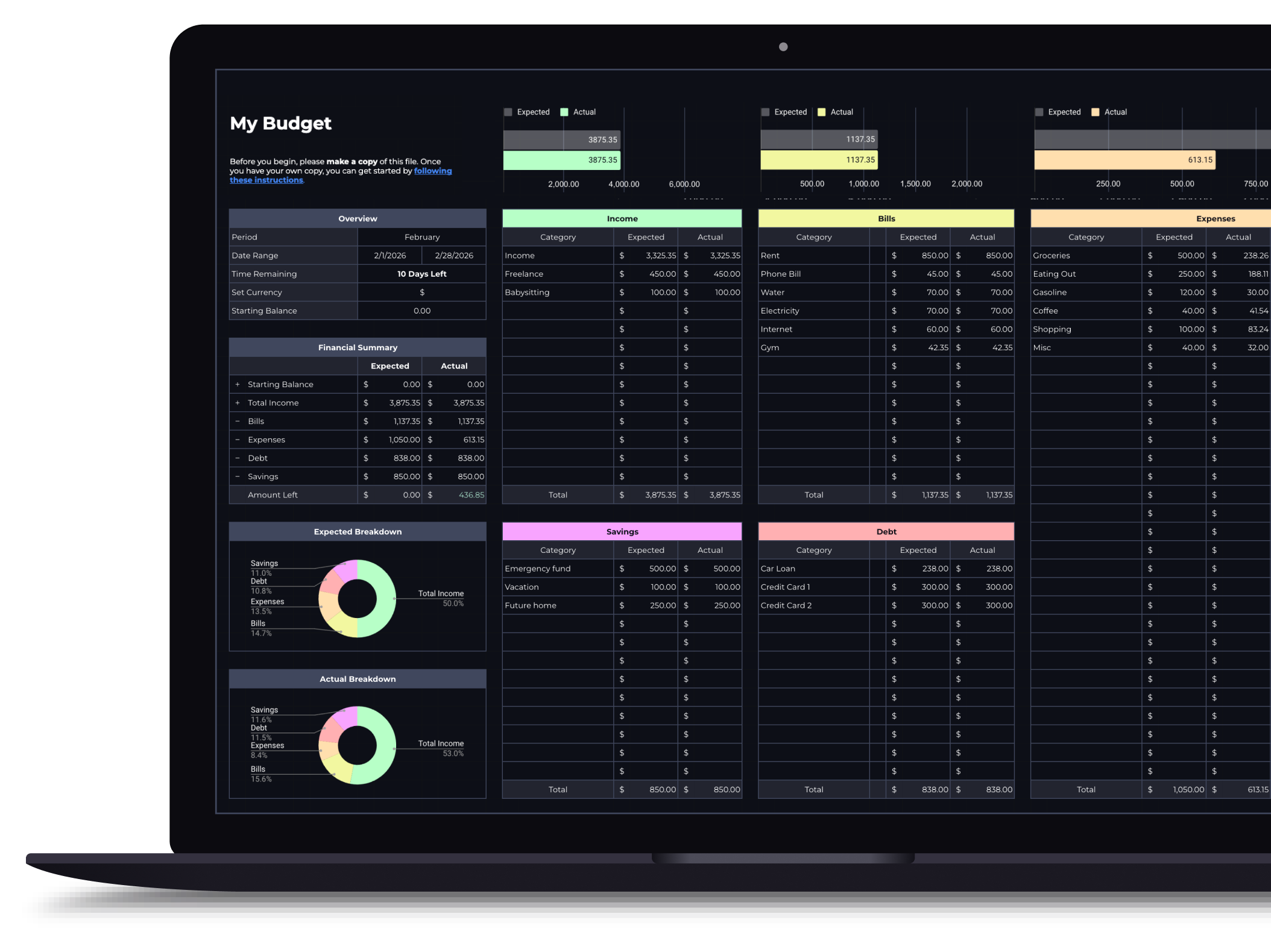

If you later decide one category deserves more detail, you can always split it. Starting simple makes it much more likely you’ll keep going. A budget template can help you organize your categories once you’re ready to formalize things.

What patterns usually appear after a month?

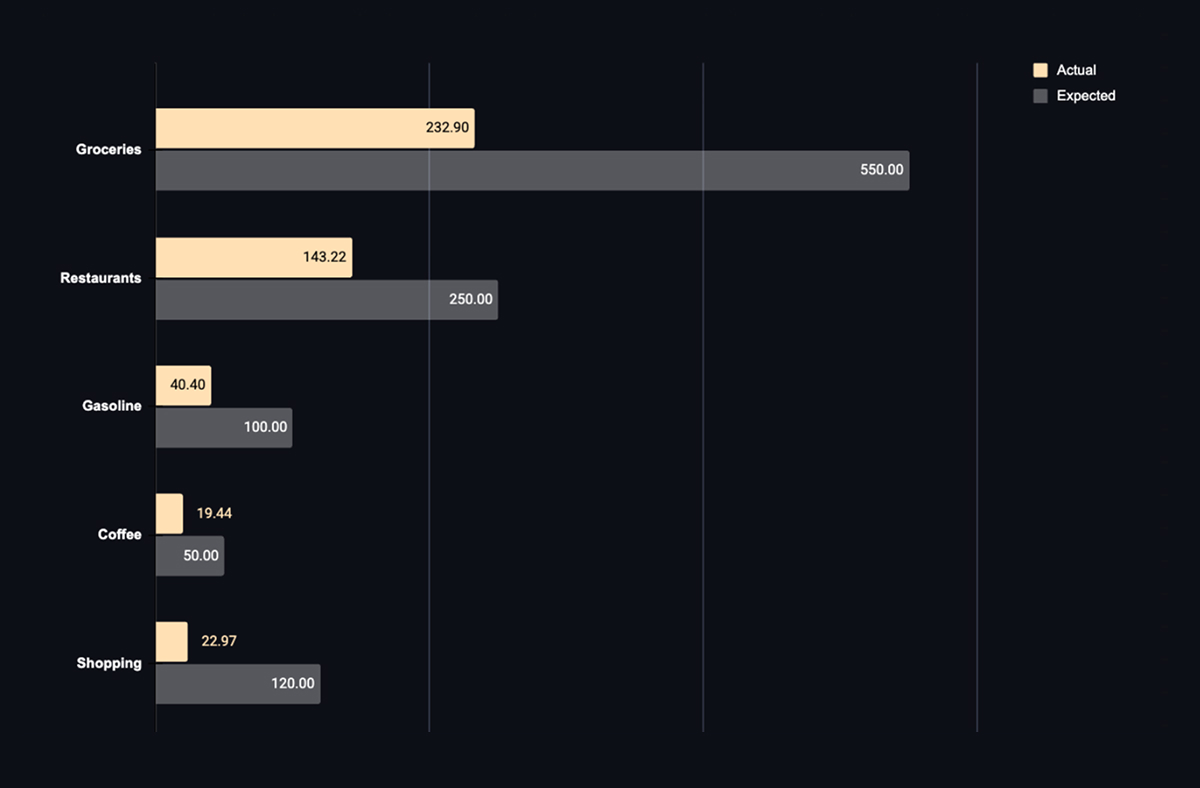

This is where tracking becomes valuable. Most people discover at least one surprise: restaurants that cost twice what they expected, subscriptions that quietly added up to far more than anyone realized, or spending that wasn’t too high overall, just inconsistent, with a few expensive weekends making the entire month feel out of control.

These patterns are almost impossible to see while you’re living through them. They’re obvious once thirty days are sitting in front of you.

That’s also why this first month shouldn’t be about judging yourself. It’s simply collecting information. Good decisions become much easier once the picture is clear. If you’ve tried tracking before and given up after a few days, tracking expenses without burning out covers how to keep going past the point where most people quit.

How do you know you’re ready to build a budget?

After thirty days, ask yourself a few simple questions.

Do you know where most of your money goes?

Can you identify your biggest spending categories?

Are there any expenses that surprised you?

Do you feel like your spending follows predictable patterns, or does it still feel random?

If you can answer those questions confidently, you’re ready to build a budget around real numbers instead of guesses.

What happens after those first 30 days?

This is where budgeting becomes much easier.

Instead of asking, “How much should I budget for restaurants?” you already know.

Instead of guessing your grocery spending, you have a month’s worth of real purchases.

Instead of wondering where your money disappears, you’ve already answered the question.

Your first budget won’t be perfect, but it will be grounded in reality instead of assumptions. That’s usually enough to make it far easier to maintain. If you’re wondering whether to rely on apps or do things manually, Awareness vs. Automation explores why the tracking method you choose matters more than most people expect. And if your paycheck lands every two weeks instead of monthly, budgeting when you get paid every two weeks covers how to line the budget you just built up with your actual pay dates.

So what’s the real first step?

Before trying to control your money, spend a little time understanding it.

Thirty days of simple expense tracking won’t solve every financial problem, but it gives every budget a much stronger foundation. The best budgets aren’t built from guesses. They’re built from habits, observations, and real numbers collected over time.